LEADERSHIP

ADF leaders play an important welfare role for those in their unit and have an opportunity to foster a culture of personal and financial discipline. Members will come to you for information and advice. Some questions will relate to their personal finances, which may include problems with debt, questions about super, salary packaging, or even for recommendations on financial products or services. Or you may become aware that a member needs assistance.

Who are we?

As part of Defence, the role of the ADF Consumer Centre is to provide financial and consumer education for members and their families. We also provide advice to the Chief of the Defence Force and Service chiefs on personal finance and consumer issues that may impact Defence members, and advise on financial education policy.

We build and maintain relationships with relevant internal and external stakeholders, for the benefit of the ADF community.

How can we help?

The ADF Consumer Centre offers face-to-face education to members at various stages of their career, typically organised by units to build financial capability for those in the unit. These sessions are supported by the online resources available on this website to help ADF members and their families.

Members are able to contact us through this website to have a specific question answered, or we can refer them to other appropriate resources.

Valuing Defence as an employer

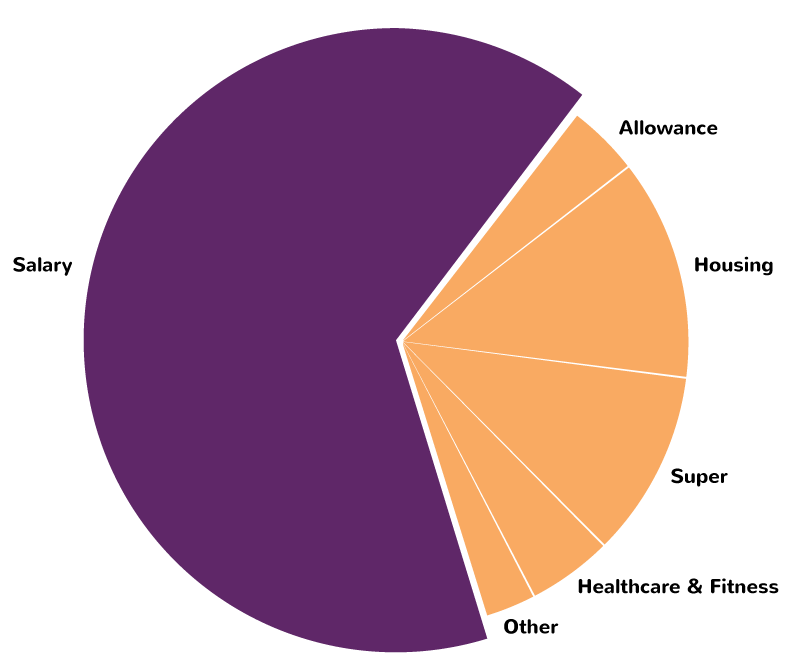

ADF members often don’t stop to think about all the additional benefits a full time career in Defence affords them. Some of these additional benefits that other employers may not provide, include:

- Additional allowances to compensate you for the unique nature of military life, such as your posting location, the performance of certain tasks or specialised skills you have, or have acquired

-

Super at a rate equivalent to 16.4% of salary and allowances, well above the minimum 12% (for those who joined for the first time after 30 June 2016)

- Death and invalidity cover at no cost, for members of the permanent forces or Reservists on CFTS, as well as DVA rehabilitation and compensation schemes

- Subsidised housing, whether living on base, off base in a service residence, or in a private rental, as well as a range of subsidies for those wishing to buy a home in their posting location

- Good sport and fitness facilities on most bases

- Free medical and dental care from doctors, dentists and nurses working in modern, well-equipped clinics and hospitals

- Uniforms and most of the equipment needed to do your job

Members can get a better idea of what their ADF remuneration package is really worth by using the employment package estimator.

The ADF Consumer Centre can help members make the most of their time in Defence, financially, by helping them develop good money habits to set them up for financial success.

Financially Fit Workforce

Being financially fit will help you set a good example for others. This short video will give you tips on how to set yourself, and others, up for financial success.

It also means having an emergency fund and insuring yourself against life’s financial challenges.

These simple steps will build your financial confidence, reduce stress and give you a better sense of well-being.

As an ADF member, being financially fit will help you focus on your role and perform at your best, and will ensure that your security clearance is not put at risk.

If you manage your money well throughout your ADF career, you’ll be more likely to achieve the financial independence in retirement that an ADF career offers.

If you manage other people, it’s especially important to set a good example as they will look to you for guidance and support.

Creating a culture of financial discipline

When members take a disciplined approach to their money they are likely to be less stressed and more able to focus on the job, making them more effective and improving the capability of the ADF as a whole. As a leader, you have a responsibility to support a culture of organisational, personal and financial discipline. You can encourage members to take responsibility for their financial affairs, starting with a budget, setting financial goals and developing a savings plan to achieve their goals.

The resources on this website will show you where to find independent, reliable sources of information to guide you along your own path and help ADF members make better financial decisions. You can direct members to the following sections on this website.

Defence members must avoid giving financial advice

ADF members are not permitted to provide financial advice to other members. Any information you give others about their finances should be factual, general in nature, and educational only.

Be careful not to express an opinion or make a recommendation about a financial service or product, as this could be perceived as advice.

For example, if you talk about banking products, insurance policies or investment products, you may talk generally about what they are and suggest places the member could find more information, but you shouldn’t mention a company or institution by name.

If you would like more information, please contact us.

Remember, it’s important that ADF members understand the difference between factual information, general assistance and financial advice, because it’s illegal for you to give financial advice without an Australian Finances Services Licence (AFSL).

Common challenges members may face

Financial difficulty

Just like the general population, sometimes ADF members get themselves into financial difficulty.

Common issues include:

- Large loans and rising interest rates

- Unexpected expenses such as car repairs or vet bills

- Salary packaged vehicles significantly reducing take-home pay

- Overuse of buy now pay later (BNPL) schemes and other forms of short-term high-interest credit

-

Sports betting and other gambling

-

Speculative high risk investments or scams

If financial issues aren’t dealt with quickly they can have serious consequences such as having possessions repossessed or getting trapped in a high-interest debt merry-go-round. This has led some members to enter into debt agreements, which, as an act of bankruptcy, can affect their security clearance and ultimately, their ongoing employment with Defence.

Members who are struggling with debt may find it harder to focus on their job. It can also affect relationships and mental health.

Help for members

People of all ages and ranks can suddenly find themselves in financial difficulty. As leaders, you can encourage them to:

-

Seek help before they default on a debt

-

Contact their credit provider to organise an extension or a repayment arrangement under hardship provisions

-

Read our problems with debt information

-

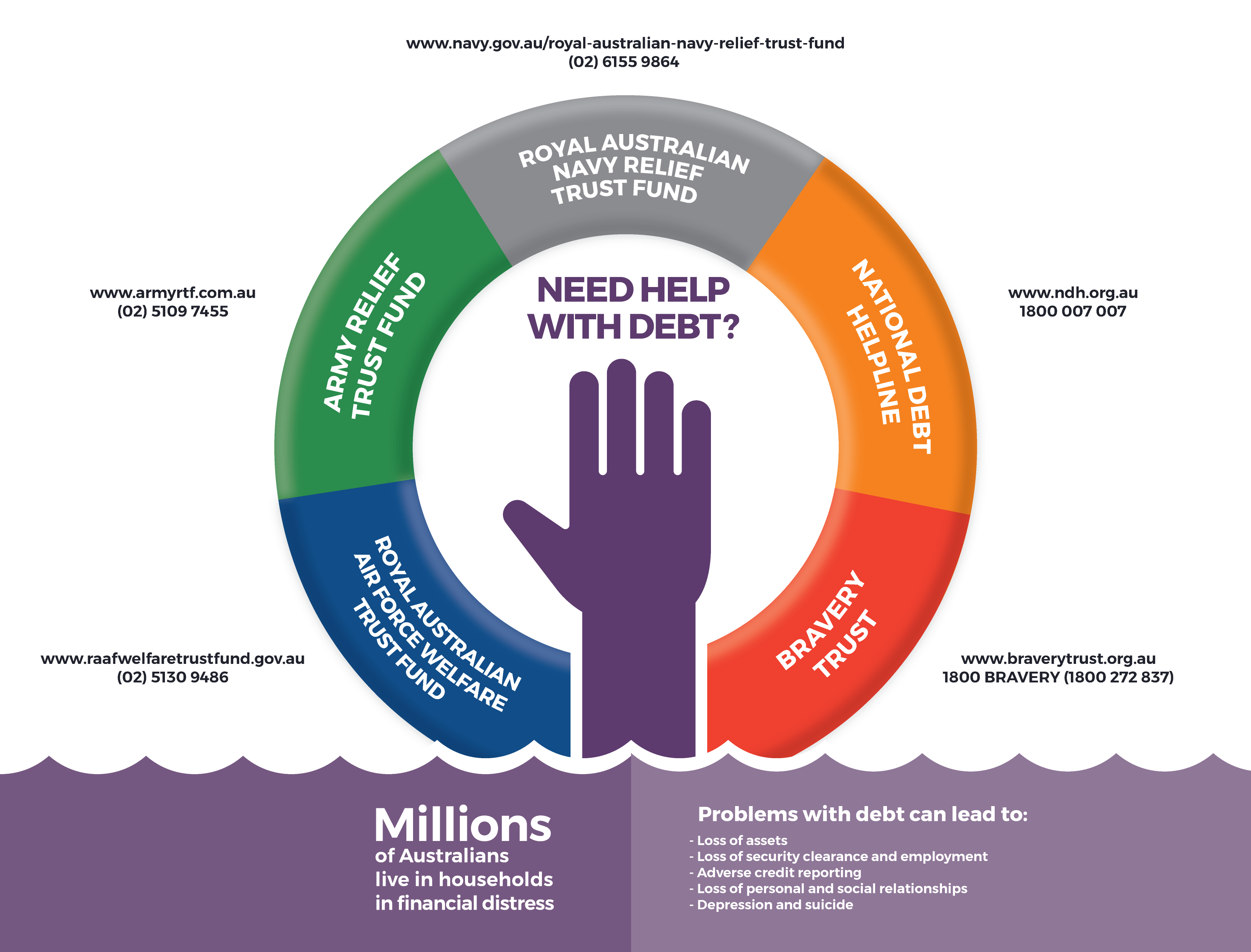

Find a free financial counsellor who can help them work through their financial issues by contacting the National Debt Helpline on 1800 007 007

-

Contact us so we can help put them in touch with a free financial counsellor

Credit reporting

One really important reason for members to stay on top of debts and pay bills on time is the effect it can have on their credit rating if they don’t. This is something that everyone should be aware of. A poor credit rating can affect your ability to access services and even borrow money in the future.

Your credit report is a comprehensive record of your credit history. It lists personal details, information about the credit products you currently have, and any credit you’ve had, or applied for, in the last 2 years. It also lists any missed or partial payments.

Credit reporting agencies use this information to give you a credit score. Lenders and other credit providers use your credit report and credit score to decide whether to lend you money, how much to lend you, and even what interest rate to charge you. People with a higher credit rating will often be able to negotiate better interest rates. Read more about Credit on our site.

It’s important to check your credit report and credit score to make sure there are no unauthorised transactions on your file. For example, someone having applied for credit in your name without your knowledge or authorisation.

You can get a copy of your credit report for free, once a year. It’s also free to find out what your credit score is. The MoneySmart website has information on how to access your credit report for free and interpret the information provided.

Assistance for members

Sometimes the best way to help a fellow ADF member is to refer them to an appropriate external service.

Centrelink’s Financial Information Service (FIS)

This is a free service which can help members with personal and family financial matters and make sure the member is getting all the Government benefits they are entitled to. The service can be accessed over the phone or face-to-face. Members can find out more information on the Services Australia website or call 132 300 to make an appointment.

Financial counselling

Financial counsellors provide a free service to help people experiencing financial difficulty. It can help a member manage their immediate crisis and develop strategies to help prevent future problems. They are able to advocate for the member and assist them to take back control of their financial affairs.

Please contact us at the ADF Consumer Centre for help in finding an appropriate financial counsellor for the member.

Financial advisers

Some ADF members have proven to be good savers and money managers and may come to you for investment advice. If this happens it’s important that you don’t make suggestions in relation to particular investment products, or classes of assets. Suggest the member read our Investing page and consider contacting an appropriately licensed financial adviser.

Financial advisers help people set and achieve financial goals, choose investments, and manage their money, for a fee.

Advisers often charge fees based on a percentage of assets under management, which can lead to conflicted advice. The ADF Consumer Centre administers the ADF financial advice referral program, which provides a list of financial advisers that have made an undertaking to Defence that they will operate on a genuine fee-for-service basis, free from remuneration-based conflicts of interest.

The list is not a recommendation or endorsement of the advisers, and members need to be aware that any relationship is between them and the adviser is a strictly private relationship that Defence is not a party to.

Members considering financial advice may benefit from reading our Getting financial advice page and watching our video Financial advisers: the facts & the fiction, which will give them a good idea of what to expect when seeing a financial adviser and what to look out for.

Before choosing an adviser, make sure the adviser is qualified to give the kind of advice the client is after and has experience in dealing with people in similar circumstances. They should understand and agree the scope of the advice and the fees before proceeding, these should be outlined in a letter of engagement.

Wills and Power of Attorney

Every Defence member should have a valid will. This is a legal document that dictates how their assets are to be distributed when they die.

For help drafting or updating a simple will for serving members, there is now a central email address to be used as a starting point, [email protected]. Members fill in a form and then a legal officer will get in touch. It’s important to keep these documents up to date.

Powers of attorney (POA) on the other hand are something they should consider carefully before granting. It’s important that members understand the implications of granting someone a POA, it’s a significant amount of power and responsibility to hand someone, so it should only be given to someone who is trustworthy and mature.

Help with tax

The Australian Tax Office (ATO) website has a tax guide specifically for ADF members, with examples on what income must be declared and what deductions are allowed. Members should be encouraged to use this guide when completing their tax via the myGov portal.

FACILITATING FINANCIAL WELLBEING CHECKLIST

SIGN UP FOR OUR MONTHLY NEWSLETTER

Receive articles on consumer tips, tax, superannuation and important news each month, helping you and your members manage finances.