NEW CONSUMER PROTECTIONS FOR BUY NOW, PAY LATER

May 30, 2025

EOFY SALES AND EMOTIONAL SPENDING: HOW TO SHOP SMART WITHOUT THE STRESS

May 30, 2025The end of the financial year, 30 June 2025, is approaching fast, however, it’s not too late to consider implementing a few practical tips that might reduce your tax bill or even increase your 2025 tax refund.

Not all of the following tips will necessarily apply to you, but at least by reviewing them you may be able to improve your, and your family’s, tax position as we enter the new financial year.

Paperwork

Now is the best time to organise any documentation you’ll need in preparing your 2024-2025 tax return. That includes bank and investment statements including for shares and exchange traded funds (ETFs), investment property records, and receipts for donations, work expenses and large medical costs.

Getting organised in advance of year end will mean that you’ll be in a position to lodge your tax return as early as possible. This is certainly something you should be aiming to do, especially if you’re entitled to a 2025 tax refund.

A word of warning…the Australian Tax Office (ATO) will pre-fill your online draft tax return with income (such as interest) that you’ve received from financial institutions, such as banks. This information is sent to the ATO as soon as possible after 30 June and should be loaded within a couple of weeks. However, it’s important to remember that if you lodge too early, your pre-filled return may not align with your personal records. Don’t assume that you can choose the lower amount shown in the ATO draft.

It’s your responsibility to disclose the correct amount, so waiting a while after 30 June to make sure your records and those of the ATO are in agreement is a wise thing to do. There’s no point in risking fines, penalty interest, amended assessments and stressful correspondence with the ATO. You can learn more about pre-filling of tax returns on the ATO website.

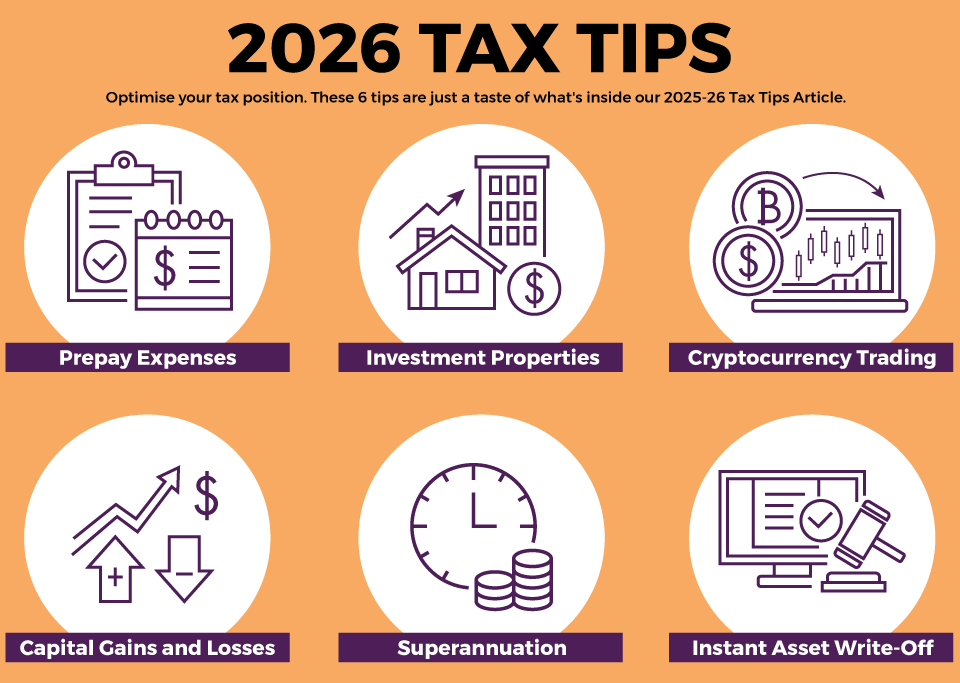

Pre-Pay Expenses

Consider pre-paying certain tax deductible expenses before 1 July. These might include professional subscriptions and certain legitimate work-related expenses.

The ATO website has a comprehensive list of work-related expenses that ADF members may claim. The list includes the conditions under which expenses can be claimed, including any required documentation. We recommend that you should review the list just in case you’ve overlooked something.

It’s important to remember that if you make a claim for a work-related expense, you must have spent the money, you must not have been reimbursed and the expense must directly relate to the earning of your income.

These criteria sound obvious enough, but many people who have not met them are identified by the ATO every year. They include people who have not actually spent the money by 30 June (or at all!) and people who have not ensured that the expense has gone through their bank account by the end of the financial year.

Make a Donation

Consider making a donation of $2 or more before 1 July 2025 to a charity of your choice that has Tax Deductible Gift Recipient status (not all charities do). Make sure you get an official receipt noting that the donation is tax deductible and ensure the amount goes through your bank account on or before 30 June. If it doesn’t, the donation will still be tax deductible, but not until the following tax year.

Investment Properties

Many ADF members and their families own an investment property. If you’re in that fortunate position, you should think about pre-paying certain costs by 30 June, such as strata fees, pest control, insurances, repairs and even some of next year’s interest. Claims against rental income arising from investment properties are under constant surveillance by the ATO so it’s important to get them right as you can see from this statement by them:

“We often see landlords making mistakes when it comes to repairs and maintenance deductions on rental properties…… we’re particularly focused on claims that may have been inflated to offset increases in rental income….performing general repairs and maintenance on your rental property can be claimed as an immediate deduction. However, expenses which are capital in nature (like initial repairs on a newly purchased property and improvements during the time you hold the property) and are not deductible as repairs and maintenance”.

The ATO website has a detailed section on tax deductible claims you can make as the owner of an investment property.

Working from Home Expenses

Claims for working from home have become more common since the Covid pandemic. The rules/methods for making these claims have changed over the years which (depending on your circumstances) may improve your tax position.

You can find out more about working from home expenses on the ATO website.

Superannuation

Here are three ways you can save tax and/or improve your family’s superannuation position by the end of the financial year:

- Establish whether you’re in a position to make (additional) tax deductible superannuation contributions (aka concessional contributions). These are limited to $30,000 for the year ending 30 June 2025. As with most issues involving tax, the rules are complex. Therefore, if you’re in a superannuation fund administered by the Commonwealth Superannuation Corporation (CSC) we recommend that you consult their concessional contribution cap estimator. If you’re not in a CSC superannuation fund, your fund’s administrator should be able to assist.

- If your spouse is not employed or is earning a low income, you may consider making an after-tax contribution to that person’s superannuation account by 30 June in order to claim a tax offset (maximum offset is $540, gradually reducing to zero when your spouse’s income is between $37,000 and $40,000). You can learn more about the conditions applying to the offset on the ATO website.

- If you earned less than $60,400 (for example, you may be working part-time), and you add money into your superannuation fund, the government may also make a co-contribution up to a maximum of $500. You can learn more about co-contributions on the ATO website.

Capital Gains and Losses

If you’ve sold any personal assets during the year ending 30 June 2025, such as an investment property or shares, any gains may be subject to Capital Gains Tax (CGT). A way to reduce the potential liability is to sell a poorly performing asset against which any capital loss can be applied to reduce (or even extinguish) the gain on which CGT is applied.

Of course, it may not be wise to buy or sell an asset purely for tax reasons. There may be other issues to consider, including the long-term purpose and value of an asset in your investment portfolio (such as its possible future use as your family home or as accommodation for children).

It’s also worth remembering that you shouldn’t assume you can simply buy back in July the assets you’ve sold at a loss in June. That action may well be considered by the ATO as an illegal tax evasion strategy. The issues in this paragraph may need advice from a licensed financial adviser and/or a registered tax agent (more on this below). You can read more about CGT on the ATO website.

Instant Asset write-off

If you and your family are running a small business (with a turnover of less than $10 million per annum), you may be able to claim an immediate tax deduction in the year ending 30 June 2025, for the full amount of all capital purchases costing no more than $20,000. Naturally, “conditions apply”. Full details and conditions are outlined on the ATO website.

Using an Adviser

Tax can be complex, so there’s a lot to be said for using the services of a registered tax agent (RTA) to prepare your tax return, or to at least seek advice on some of the technical issues raised in this article. There is a public register of RTAs maintained by the Australian Government’s Tax Practitioners Board. Most RTAs are qualified accountants, but not all qualified accountants are RTAs.

You might also consider seeking wider strategic investment/wealth/financial planning advice from a licensed financial adviser. Before you do that, we recommend reading the Getting Financial Advice section of our website which contains a link to licensed financial advisers who only charge on a fee for service basis (no commissions or percentage-based fees).

Our last point, but by no means least, is to have a clear understanding (preferably in writing) of the scope and cost of the professional advice you’re seeking. And remember to ask your adviser whether some or all of these fees will be tax deductible, preferably in the year ending 30 June 2025.

{kind=link}

{kind=link}

{kind=link}