Role of AI in Investing

September 7, 2023

FINDING A FINANCIAL ADVISER – IT CAN BE QUITE A MISSION

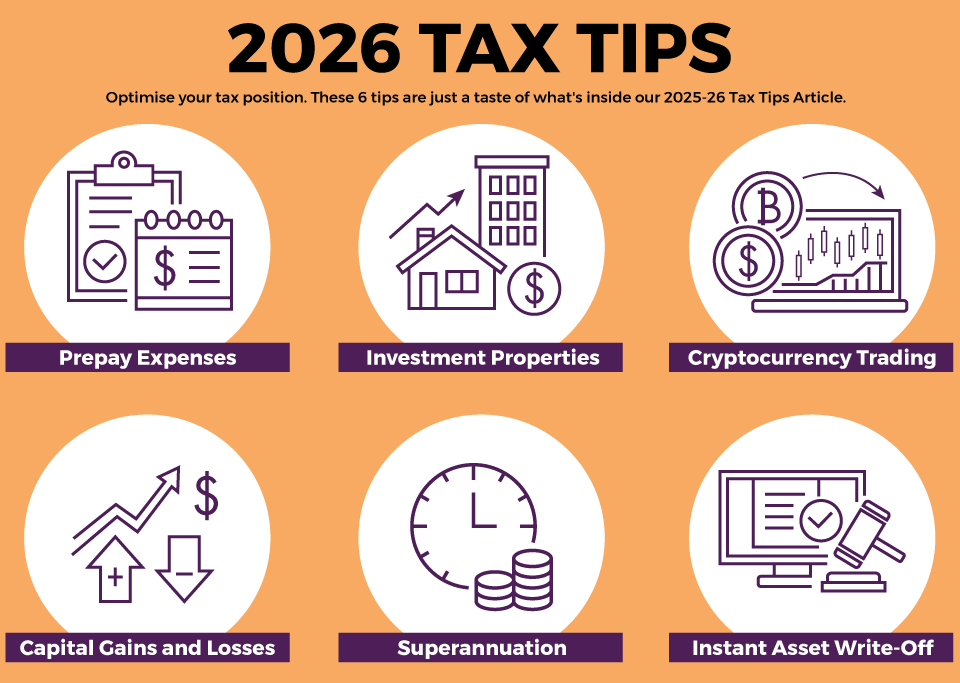

October 12, 2023Given the imminent 2023 tax return deadline for lodgement of your tax return, the Australian Taxation Office has issued some important reminders to taxpayers about their responsibilities and the areas to which special attention will be paid this year:

Lodgement deadline

As always, the lodgement deadline for people who prepare their own tax return is October 31. If you miss the deadline, the maximum penalty is a maximum of 5 penalty units of $313 each. Therefore, the maximum penalty is $1,565.

Imposition of the penalty

History shows (depending on your circumstances) that the ATO may waive a penalty for late lodgement where you’re entitled to a refund, but you won’t know that until you’ve received your annual Notice of Assessment. So the message is to lodge on time.

Use of a tax agent

If you plan to use a registered tax agent (RTA) you may have until May 2024 to lodge your tax return. However, it’s important to note is that you will only qualify for an extension of time if you have registered with an RTA by October 31.

Working-from-home expenses

A significant change in 2022-23 is the way taxpayers can claim working-from-home expenses. The old shortcut method of claiming 80c per hour has been replaced by a new fixed rate of 67c per hour with additional substantiation requirements. You can find out more on the Australian Taxation Office website.

Removal of low and middle income offset

This important and little known change in 2022-23 means that for most people their refund will be reduced or they will find themselves unexpectedly having to pay additional tax. If you’d like more details on this and how it might apply to you, read our 2023 Tax Returns and Refunds article or visit the ATO website.

Rental properties

The ATO has given notice that a particular area of focus this year will be the full disclosure of rental income by investors and the proper calculation of claims such as depreciation, repairs and maintenance and interest expenses on loans. Where part of a loan has been used for private purposes, such as buying a car or going on an overseas holiday, the interest on that private portion of the loan is not tax deductible. Any incorrect claims will be disallowed and penalties are likely to be levied.

Data Matching

These days, the ATO has extensive access to data from financial institutions, including lenders. Therefore, the chances of being caught out for making dishonest or accidental mistakes is high, as are the penalties. So it’s worth making the effort to do the job honestly and with careful attention to detail. If you don’t, you may well become a target of personal attention by the ATO for many years to come (we all like to be noticed, but not that much).

{kind=link}

{kind=link}

{kind=link}