June 29, 2026

June 29, 2026

June 19, 2026

June 3, 2026

Any bonus paid to an employee in Australia, including the continuation bonus paid in the ADF, will be taxed as income on top of a member’s […]

June 3, 2026

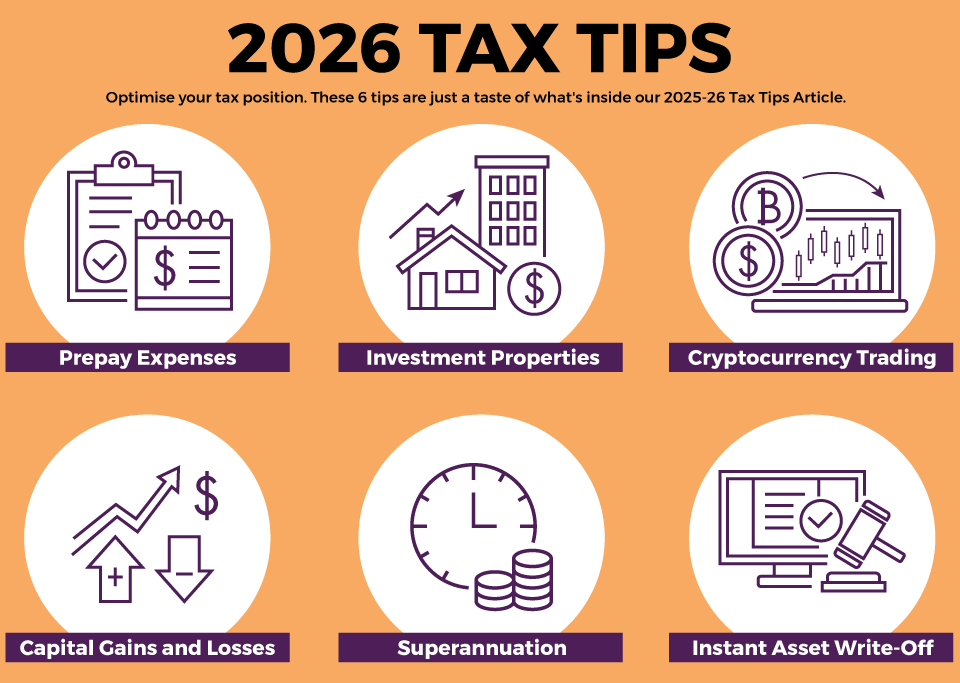

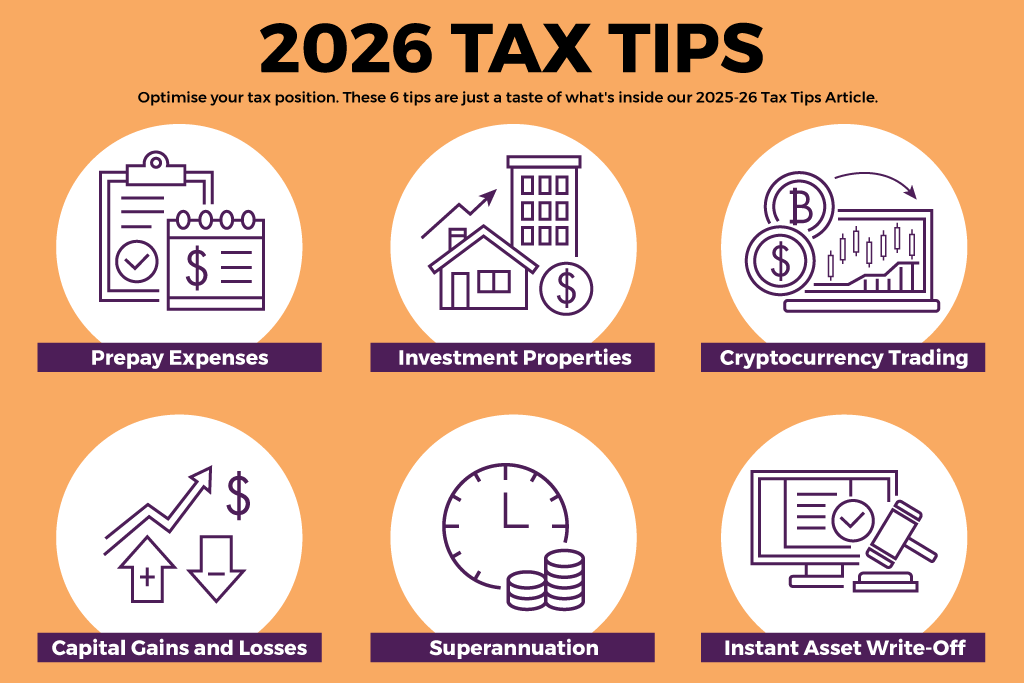

This article is written specifically for Australian Defence Force (ADF) members and their families this 2026 Tax Time, covering the 2025–26 financial year. Inside you’ll find […]

May 5, 2026

It’s the same supermarket, maybe the same day of the week. Definitely the same route through the aisles. Putting the same brands in the trolley, paying […]

May 5, 2026

This month we are focusing on managing the household budget. One item of expenditure that has escalated in recent years and is unavoidable are family healthcare […]

May 5, 2026

The Household Expenses section of our Budget Calculator is where a lot of surprises live. And right now, there are plenty of them. A family of […]

March 30, 2026

Long gone are the days when ADF recruits were automatically enrolled in the Military Superannuation and Benefits Scheme (MSBS aka MilitarySuper). With the limited exception of […]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}